The Data India Avoids — Credit Failure, Corporate Defaults, and Policy Drift

By Vijay Gaikwad | Senior Agricultural Journalist

Do Loan Waivers Actually Work? The Evidence Is Uncomfortable

The debate around farm loan waivers is often driven by emotion and political urgency. But when examined through the lens of institutional research, the conclusions are far less reassuring.

The Reserve Bank of India has studied loan waivers extensively, and its findings are sobering. A 2019 RBI working paper noted that loan waivers tend to create what economists call a “moral hazard.” When borrowers begin to expect periodic waivers, repayment discipline weakens. At the same time, banks — anticipating higher default risks — become more cautious in extending fresh credit to agriculture.

The result is paradoxical. A policy designed to support farmers can end up restricting their future access to institutional finance.

As the RBI observed:

“Loan waivers do not address the root cause of farm distress — they merely postpone it, while simultaneously weakening the institutional fabric of agricultural credit.” — RBI Working Paper, 2019

The National Bank for Agriculture and Rural Development (NABARD) has echoed similar concerns. Its research has consistently emphasised that what farmers need is not periodic debt forgiveness, but sustained improvements in income — through better price realisation, reduced input costs, irrigation investment, and access to affordable credit.

Global institutions have also flagged the issue. Both the World Bank and the IMF have pointed out that large-scale loan waivers impose a fiscal burden on states, often reducing their ability to invest in long-term agricultural infrastructure — precisely the investment that could prevent distress in the first place.

The Data India Avoids: Wilful Defaulters

There is, however, another side to the credit story — one that receives far less public scrutiny.

Over the past decade, India has witnessed a dramatic rise in wilful defaulters — borrowers who had the capacity to repay but chose not to. The scale of this increase is not incremental. It is exponential.

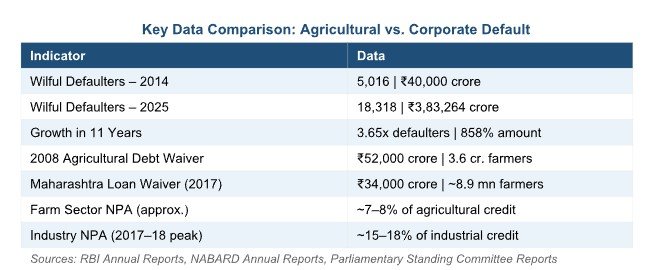

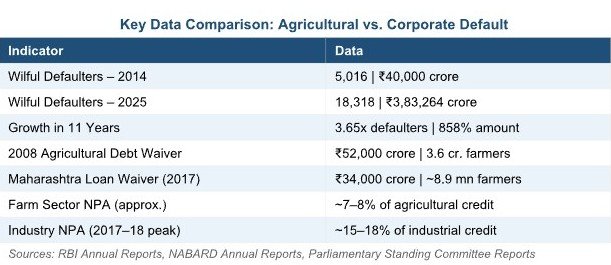

In 2014, India had just over 5,000 wilful defaulters with outstanding dues of around ₹40,000 crore. By 2025, that number had grown to over 18,000 wilful defaulters, with dues exceeding ₹3.8 lakh crore.

The growth is not merely numerical. It reflects a deeper failure within the banking system — one that raises questions about credit appraisal, regulatory oversight, and accountability.

The comparison with agricultural debt is unavoidable.

India’s largest farm loan waiver — the 2008 scheme — amounted to ₹52,000 crore and benefited millions of small farmers. The outstanding dues of wilful defaulters today are several times that amount.

Yet the policy response to these two categories remains fundamentally different.

The Moral Imbalance in India’s Credit System

The distinction between a farmer in distress and a wilful defaulter is not just economic. It is moral.

A farmer defaults because of factors beyond his control — failed monsoons, crop loss, price crashes. A wilful defaulter defaults despite having the means to repay, often after diverting funds or restructuring liabilities strategically.

And yet, the consequences they face are starkly unequal.

The small farmer encounters recovery notices, social pressure, and in extreme cases, personal tragedy. The corporate defaulter enters a legal process, negotiates settlements, and often exits with reduced liability under structured mechanisms.

This asymmetry has eroded trust in the financial system.

It has also distorted the public narrative — where agricultural distress is treated as a fiscal burden, while large-scale corporate default is absorbed as a systemic cost.

Also Read: Farm Loan Waivers: Relief or Political Illusion? Inside India’s Agrarian Crisis

Institutional Failure and the Question of Accountability

The rise of wilful defaulters is not an accident. It is a symptom of institutional failure.

Public sector banks, entrusted with safeguarding depositor and taxpayer money, have repeatedly extended large exposures to corporate entities without adequate safeguards. In many cases, lending decisions were influenced by factors that went beyond financial viability.

Enforcement mechanisms have been slow, selective, and often reactive. While agencies such as the Enforcement Directorate and the Central Bureau of Investigation have taken action in high-profile cases, the pace of recovery remains disproportionately slow compared to the scale of default.

What is missing is transparency.

India needs a comprehensive public accounting of wilful defaults — who borrowed, how much, what was recovered, and what remains outstanding. Without this clarity, the debate on farm loan waivers remains incomplete.

Artificial Intelligence in Agriculture: Promise and Peril

Even as traditional challenges persist, Indian agriculture is entering a new phase shaped by technology.

Artificial Intelligence promises precision farming, better weather prediction, improved yield forecasting, and more efficient input use. Startups are deploying AI-driven advisory platforms, drone-based monitoring, and satellite-based analytics to transform decision-making at the farm level.

But the risks are equally significant.

Agricultural data — soil health, crop patterns, market behaviour — is becoming a valuable asset. In a country where the majority of farmers are small and marginal, there is a real danger that control over this data could shift to large corporations or platform owners, creating new forms of dependency.

Technology, if not carefully regulated, can replicate existing inequalities in a more sophisticated form.

The challenge for policymakers is not merely to promote AI adoption, but to ensure that it empowers farmers rather than displacing their agency.

From Relief to Reform: The Missing Policy Shift

The recurring reliance on loan waivers reflects a deeper policy inertia.

Long-term solutions — irrigation infrastructure, market reforms, supply chain integration, and income diversification — require sustained investment and political continuity. They do not produce immediate headlines. They do not align neatly with electoral cycles.

Loan waivers do.

That is why they persist.

India’s agricultural policy, for too long, has favoured visibility over viability. The result is a system where distress is addressed repeatedly, but rarely resolved.

Conclusion: The Crisis of Political Will

The Indian farmer is not asking for periodic relief. He is asking for a system that works.

He needs fair prices, reliable water, accessible credit, and functioning markets. He needs policy stability, not episodic intervention.

Loan waivers may ease immediate distress, but they cannot replace structural reform.

The next time a loan waiver is announced, the question should not be how much is being waived. The question should be whether it will still be necessary five years from now.

If the answer is yes — and it often is — then the problem has not been solved.

It has only been deferred.

Editor’s Note

At TheNews21, our ongoing “World Bank Loan Trap” investigation has documented how large-scale financial interventions, aimed at strengthening farmer resilience, have often failed to deliver structural outcomes on the ground. The gap between policy design and field reality remains significant.

Loan waivers, in many ways, operate within that same gap — offering visible relief, while leaving deeper systemic issues unresolved.

{kind=link}