Audit says departments sought additional funds despite failing to utilise original budget allocations; ₹1.37 lakh crore in supplementary provisions ultimately proved excessive

The CAG has questioned Maharashtra’s budget planning after finding ₹29,742 crore in unnecessary supplementary grants and observing that ₹1.37 lakh crore in supplementary provisions ultimately proved excessive during 2024-25.

Mumbai: The Comptroller and Auditor General (CAG) has raised serious concerns over Maharashtra’s budget planning after finding that supplementary grants worth ₹29,742.51 crore sanctioned during 2024-25 were unnecessary because the concerned departments did not even utilise their original budget allocations.

The findings, contained in the State Finances Audit Report tabled in the Maharashtra Legislature, also show that supplementary provisions amounting to ₹1,37,066.48 crore ultimately proved excessive, pointing to significant weaknesses in expenditure forecasting, budget preparation and financial management.

Under the Constitution and the Maharashtra Budget Manual, supplementary grants are intended to provide additional funds only when expenditure cannot be met from the original budget allocation or through reappropriation. They are expected to be sought only after departments establish that the original provision is genuinely insufficient.

However, the CAG found that in 62 grants and appropriations, supplementary provisions aggregating ₹29,742.51 crore were sanctioned even though the actual expenditure during 2024-25 failed to reach the level of the original budget provision itself. According to the audit, these supplementary grants were therefore unnecessary.

The report further states that in 84 grants and appropriations, supplementary provisions amounting to ₹1,37,066.48 crore proved excessive because the final expenditure remained substantially below the total funds made available after the additional allocations were approved.

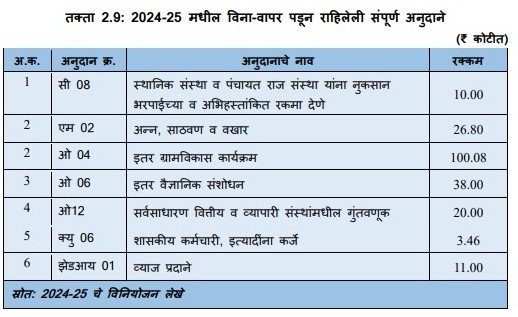

To illustrate the pattern, the CAG cited six major cases where supplementary provisions exceeding ₹1,000 crore each were sanctioned even though the departments ultimately spent less than their original budget allocations. The audit said these examples reflected unrealistic expenditure projections and weak financial planning.

The report also highlighted specific instances where departments obtained supplementary allocations but later recorded substantial savings. In one case, a department received an additional provision of ₹56.88 crore for biodiversity-related activities but eventually spent only ₹14.50 crore, resulting in savings exceeding ₹102 crore. The department attributed the savings to vacant posts, lower-than-expected expenditure, non-receipt of bills and non-completion of planned works.

In another case relating to the Water Supply and Sanitation Department, supplementary provisions were sanctioned even though the department ultimately recorded savings of more than ₹1,600 crore against the total funds available.

According to the CAG, the pattern indicates deficiencies in budget estimation, scrutiny of supplementary demands and expenditure monitoring during the financial year. Seeking additional funds that are ultimately not required weakens legislative financial control and affects the credibility of the budgeting process. The audit observed that such cases reflected inadequate budget realism, insufficient scrutiny of supplementary proposals and weak expenditure management across departments.

The CAG has recommended that the State Government strengthen budget preparation, improve monitoring of expenditure throughout the financial year and ensure that supplementary demands are placed before the Legislature only where additional funds are genuinely required. Better financial planning, it said, would improve fiscal discipline and enable more efficient utilisation of public resources.

{kind=link}